Configure Credit Line Increase (CLI) policy on the Platform¶

Overview

Proactive customer line management strategies can be a key retention tool and competitive differentiator for banks, if banks are able to execute their CLI strategies, refinements and deployment processes well.

A key element of execution is the need for banks to be agile in its CLI strategies to competitive moves in the marketplace and robust monitoring of existing lines to identify opportunities proactively. In addition, as need for changes are identified, banks need to move their strategies from analytics to production quickly while maintaining strict governance and robust compliance (ex: biases in decisions from updated strategies). This process needs to work iteratively as best-in-class vis-a-vis peer banks to create sustained advantage.

This is where Corridor Platforms, as the Decision Management ‘rails’ for CLI strategies can be a strategic enabler of competitive differentiation in the digital marketplace.

Developing a CLI Strategy

The use case, showcases the development of a full blown CLI customer management policy on Corridor Platforms which leverages a sophisticated customer value framework and optimization strategy to create a custom CLI offer for existing credit card customers of the bank. The strategy also includes a customer eligibility criteria for CLI as well as a ‘knock-off’ or limits strategy to prune the optimized offers based on the banks risk tolerances.

Corridor has the ability to develop this policy at the customer level and hence manage the customer level exposure proactively and transparently from a risk/reward perspective.

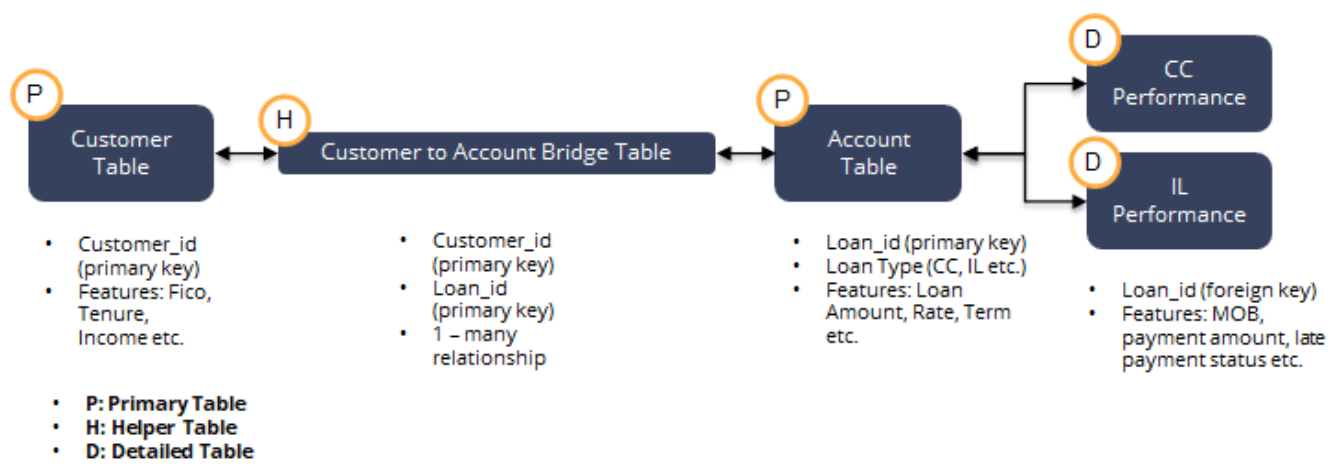

Step 1 - Setup the data model in Corridor to capture the customer footprint flexibly

To capture the customer footprint, the platform offers a flexible entity structure to map data from disparate sources in the customer lifecycle, like Customer, Loan and Performance tables. The platform also allows the policy writer to create custom entities (ex: segment) to roll up data on custom dimensions for features as well as powerful reporting on strategy performance.

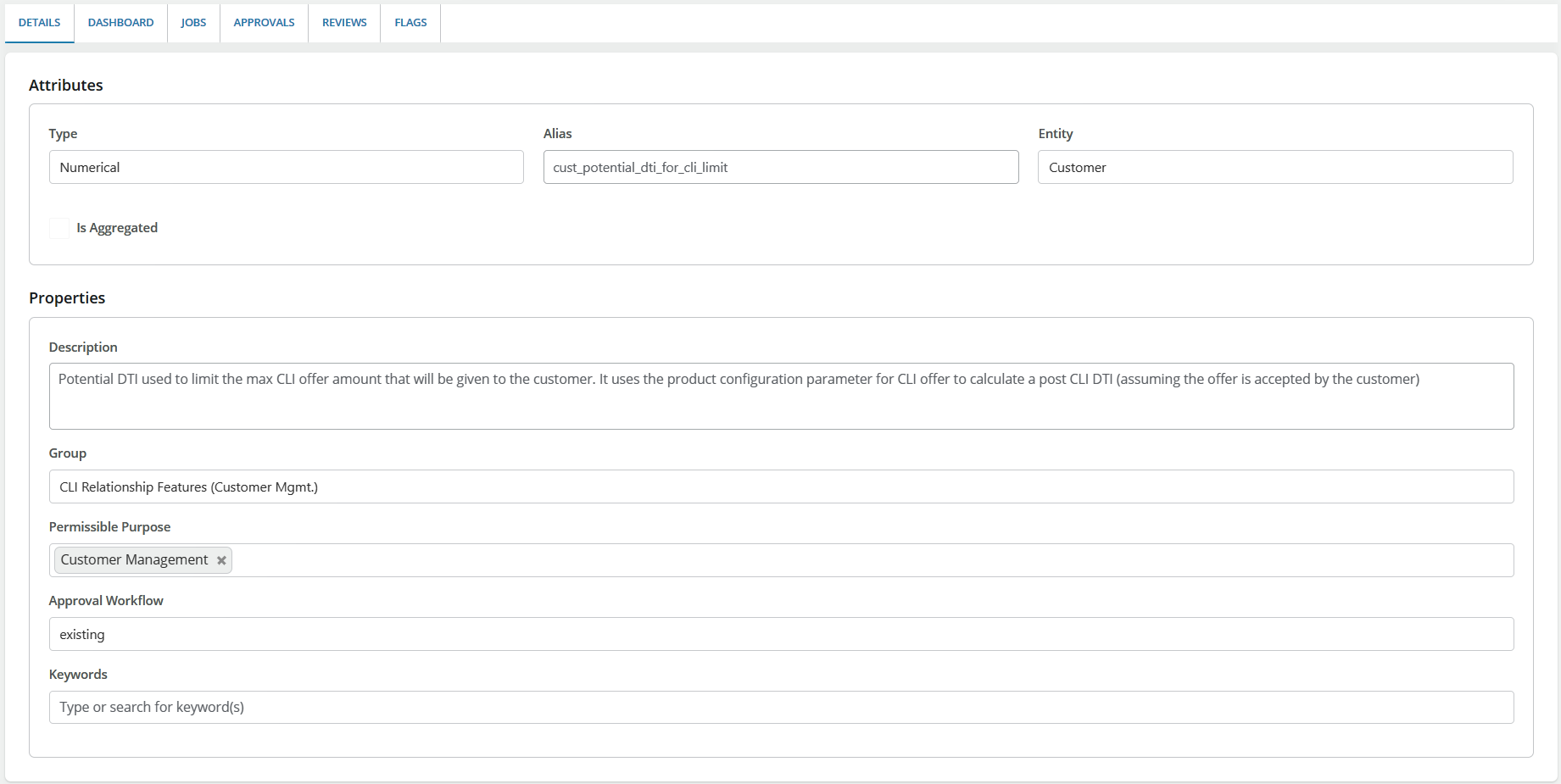

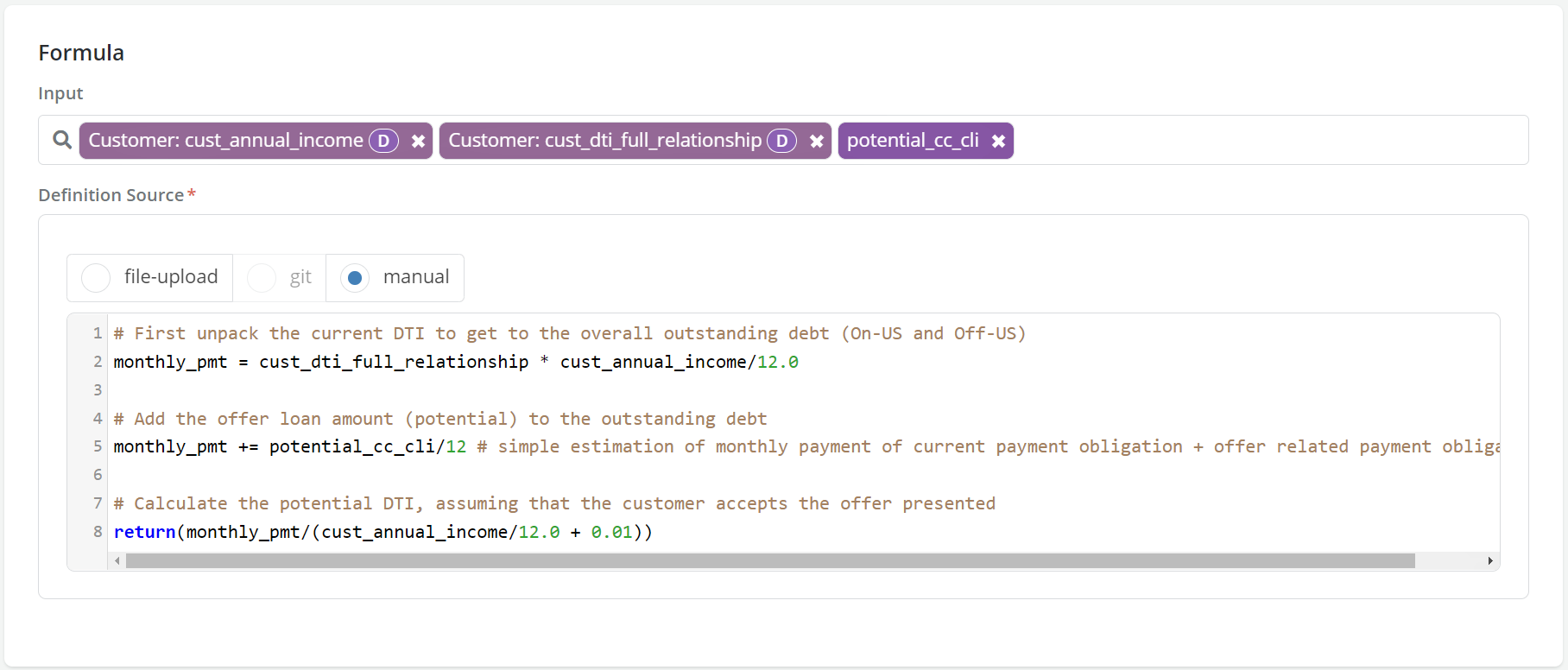

Step 2 - Creating powerful customer level features for CLI

Post the mapping of the tables and their relationships, build customer level features leveraging data across the relationship including complex aggregations and features based on offer related parameters. As an example, the feature below is used in a ‘limits’ strategy to calculate the max offer that can be given to the customer which does not breach the Debt-To-Income risk tolerance setup by the bank.

Similarly, the policy writer can create powerful features based on the relationship footprint of the customer using data across different sources to develop relevant strategies, some examples are:

- Earliest credit line opened with the bank (On_US)

- Number of delinquencies in existing credit lines over last 6 months (On_US)

- Total outstanding debt balance across all banking relationships (On_US + Off_US)

- The platform is able to stitch decision strategies easily and automatically across these disparate sources of data and provide an artifact for scoring, without the policy writer needing to manually stitch the solution together.

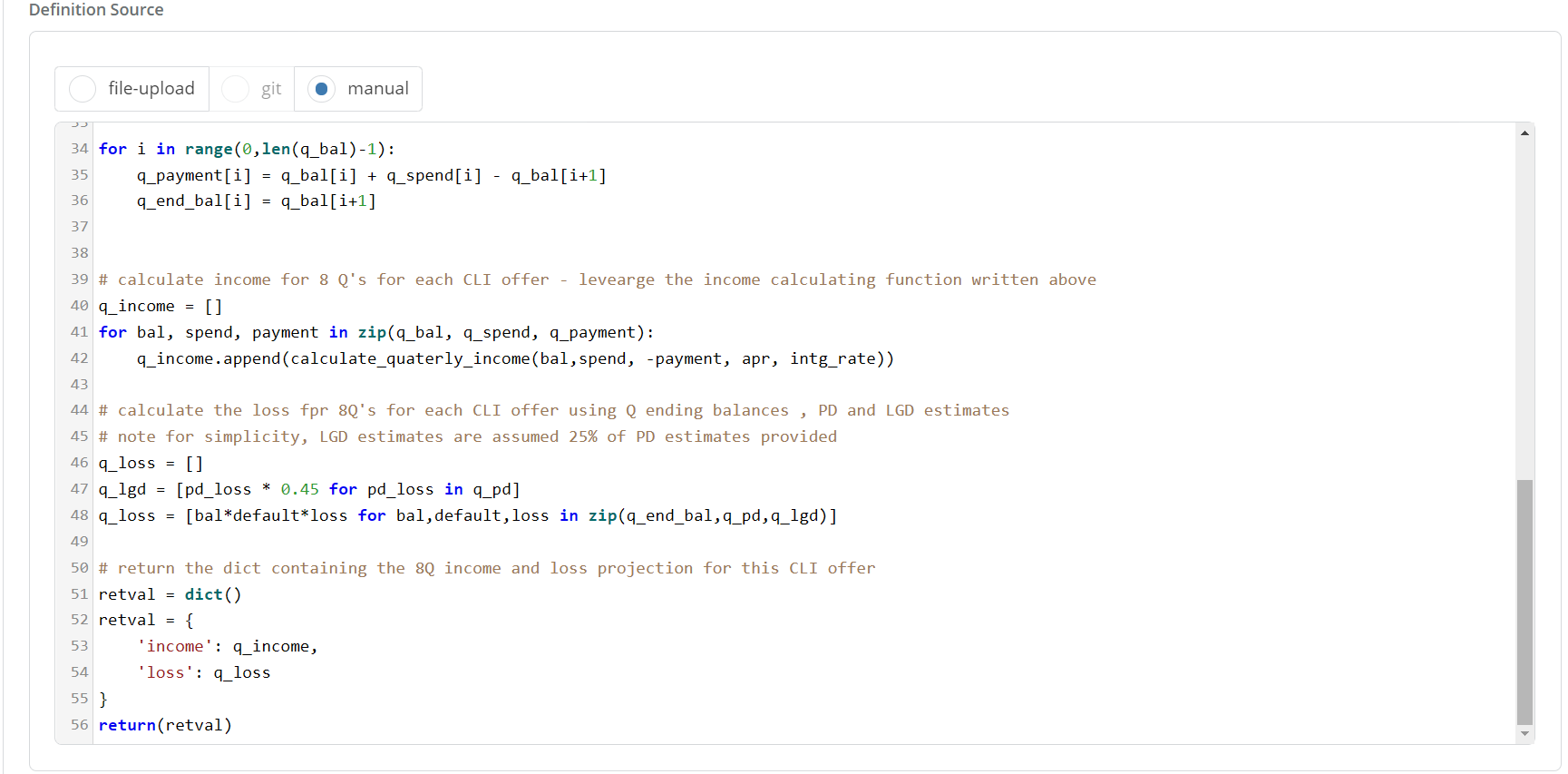

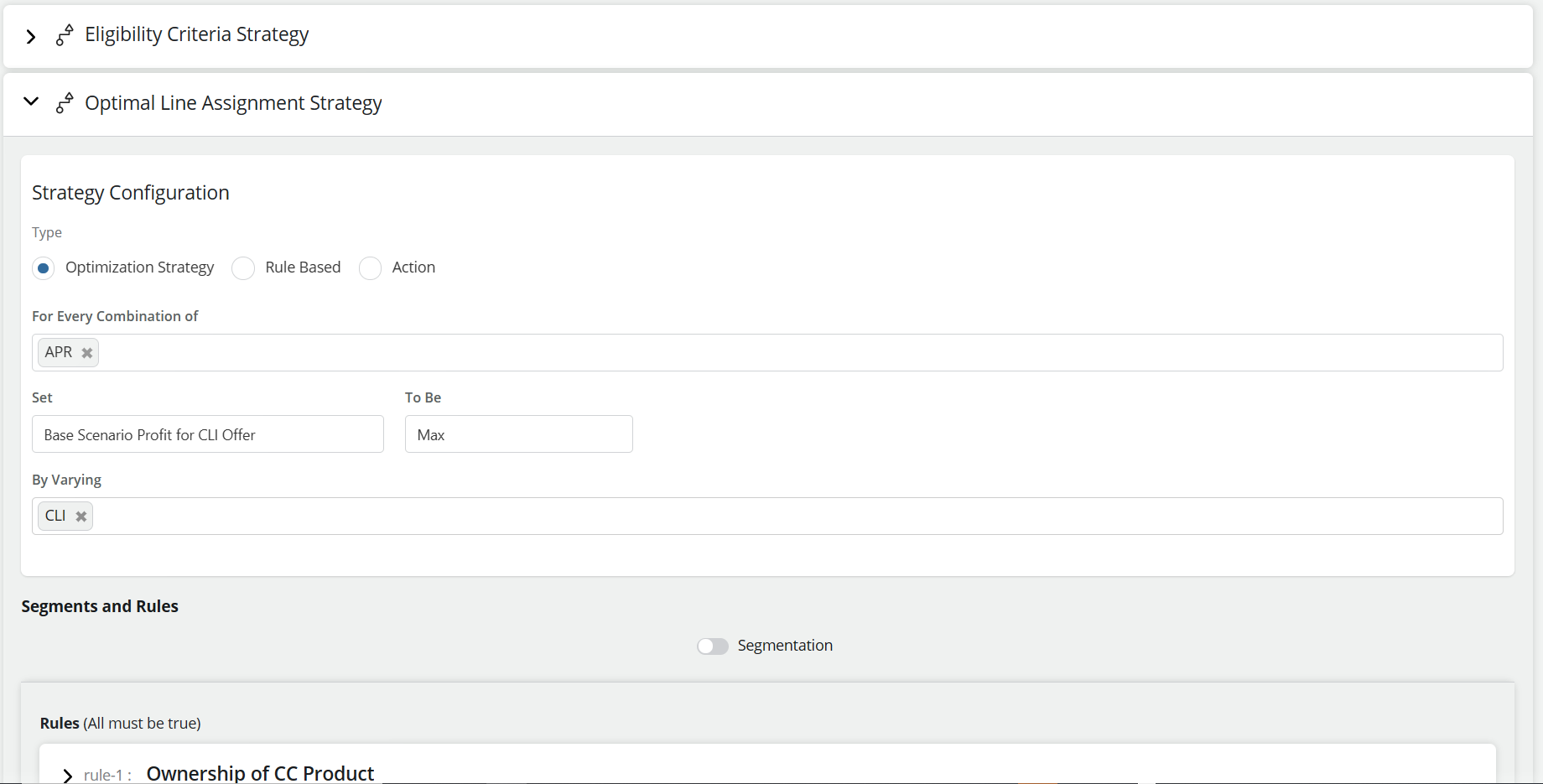

Step 3 - Creating an optimization framework for CLI offers

Set up a sophisticated custom framework on the platform to calculate the estimate of customer value if the CLI offer is taken up by the customer. The platform allows the policy writer complete flexibility in defining a custom logic. An illustration of such logic coded on the platform as a framework is below:

In the example above, the framework takes the following category of inputs and produces an estimate of customer value (or profit).

-

Framework inputs:

- Fixed inputs to calculate revenue streams (ex: APR)

- Forecasts of credit card balances and estimate losses over a predefined period.

-

Framework outputs:

- Estimate of customer value (or profit) which will be used in the CLI strategy (see below) to choose the best offer

Step 4 - Develop a CLI strategy which leverages the features, models and framework on the platform

Define a sophisticated optimization strategy which can execute in real-time to cycle through a set of offers generated on the platform, and in this case, find the one offer which maximizes profit potential while offering the customer a CLI inline with their needs. You can also write decisioning logic for eligibility criteria and limit strategies to prune the set of customers and offers respectively before presenting them through downstream systems.

Step 5 - Stitch the artifact together for real time deployment easily on Corridor with flexible deployment options

The platform automatically stitches together the entire decision artifact consisting of data, features, models, decision strategies as a standalone artifact which can be deployed flexibly in the banks.

Step 6: Testing real time execution scenarios for CLI offers

The platform also supports various options to experiment with policy decisioning & testing prior to final approvals. One capability is ‘single-record’ run which runs the real-time artifact for single customers as a way to test logic and iron out edge case issues. The platform provides full decision traceability to support debugging the policy prior to final deployment.